Oroco Resource Corp.

Oroco Resource Corp. is a Canadian mineral explorer that owns a majority interest in the Santo Tomas porphyry copper deposit in Sinaloa, Mexico. Although that’s not the only project Oroco is involved in, it’s by far their biggest and what we’ll be focusing on in this blog. This will be an introduction and overview, not an exhaustive report. To truly understand Oroco and the Santo Tomas copper project, spend time reading the drill reports and source material.

SANTO TOMAS OVERVIEW

Pounds: 8.7 billion pounds CuEq (copper equivalent) in all categories

Average CuEq grade: 0.36%

Strip ratio: 1.16

KEY TAKEAWAYS

Oroco owns an 85.5% stake in the Santo Tomas copper project located in a historically friendly mining jurisdiction in Sinaloa, Mexico.

The PEA released in October 2023 returned an after-tax NPV8% of US$1.2B and an IRR of 17.3%, confirming the economic viability of the project.

Average CuEq grade of 0.36%, but lower operating costs from being in a low elevation area and ease of access to nearby cities and ports make the low grade feasible.

Oroco trades at C$0.50 as of this writing, with a market cap of C$120M (US$0.37, US$90M market cap). With the recent PEA results, its stake in Santo Tomas is worth about C$675M (US$500M). This means it currently trades for less than 20% of the potential selling price.

There is upside available with more drilling to further expand and de-risk the project, as well as if copper prices increase.

Copper is expected to be in a supply deficit for the latter half of this decade, and there are few mines of Santo Tomas’ caliber available to close the gap.

Led by well-regarded management team of mining executives with experience in successful exploration.

WHAT IS SANTO TOMAS?

Santo Tomas is located in Sinaloa State, Mexico, about 100 miles from the coastal city of Los Mochis. It sits in a friendly mining jurisdiction on the Laramide belt, a long porphyry copper belt that extends from Arizona and New Mexico down through western Mexico with a number of high quality copper deposits throughout the belt.

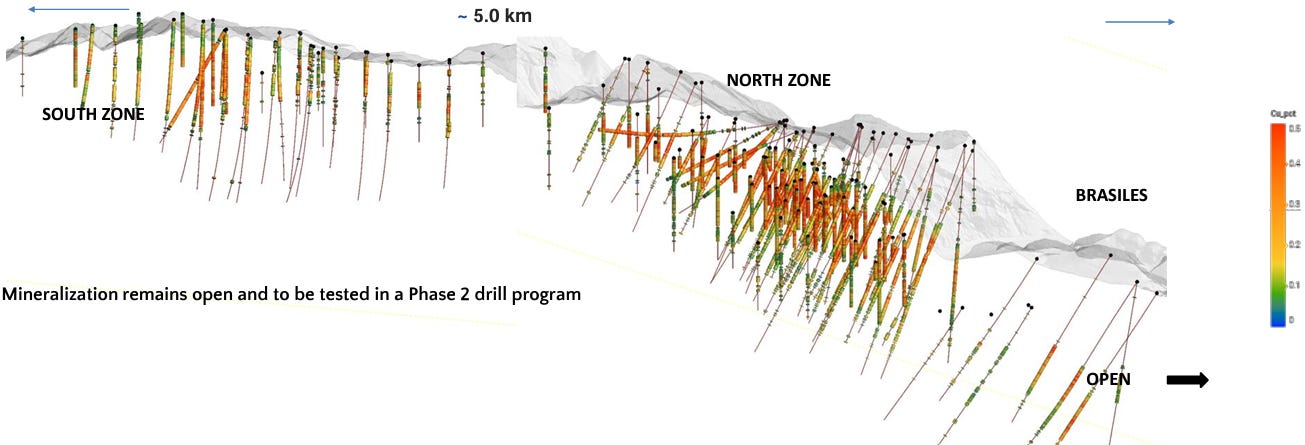

Santo Tomas consists of three zones - North, South, and the lesser explored Brasiles. The river in the below picture is the Rio Fuerte, which serves as the border between the states of Sinaloa and Chihuahua.

EXPLORATION AT SANTO TOMAS: 1968 - 1994

Santo Tomas was explored sparsely from 1968 to 1994, with the first round of drilling done by ASARCO, who completed a drill program consisting of 43 core holes, mainly in the North Zone. A couple holes were drilled with successful results in the South Zone, but not enough to provide a picture of the underlying deposit. After ASARCO completed their drilling, a couple other companies did more drilling to extend the known mineralization area and fill in some of the gaps in the drill hole pattern to gain more confidence. Then Santo Tomas sat undisturbed for almost 20 years.

Bateman Engineering of Tucson, Arizona was contracted by Exall Resources in 1994 to complete a pre-feasibility study, which produced a positive result, but focused on the North Zone and largely ignored the South Zone. All the work done to this point showed favorable metallurgical results, but ignoring the South Zone and not drilling deeper in some areas meant there still lacked a complete picture of the Santo Tomas deposit.

OROCO GETS INVOLVED: 2017 - PRESENT

The 1994 pre-feasibility study was the last notable work done on the project until Oroco got involved in 2017. They used the historical drilling results to conduct an evaluation and geological mapping of Santo Tomas. Then they gained a majority interest in the project in 2018.

In 2020, they conducted a 3-D resistivity and induced polarization (IP) survey on 10 square kilometers across all three zones - North, South, and Brasiles. A 3D-IP survey essentially aims to identify the chargeability of the metal underneath the surface without doing any drilling. It provides you a map of what could be beneath the surface and can help identify where to drill.

OROCO BEGINS DRILLING

Oroco compared the 3D-IP results to the historical drill results and found a correlation, and used this to go ahead with their own drill program. They began their drill program in July 2021 and finished in March 2023. In total they drilled 76 holes in Santo Tomas - 48 in the North, 21 in the South, and seven in the unexplored Brasiles Zone. Then, Oroco contracted Ausenco in Tucson, Arizona to conduct the Preliminary Economic Assessment (PEA), which was released on October 11, 2023.

If you’re unfamiliar with mining, a PEA is a giant report done by an independent third-party to assess the economic viability of a project, specifically the profitability potential and risks involved. It provides credibility to the project, and gives prospective investors insight into the investment’s attractiveness and the return potential. Investors may want to look further into the risks outlined in the PEA, such as environmental or geopolitical risks. For Santo Tomas’ purposes, the PEA outlined how much copper is in the ground, and roughly how much it will cost to get it out.

PEA RESULTS

The seven holes drilled in the Brasiles Zone were excluded from the PEA since the Brasiles is largely still unexplored, making it difficult to assess the economics for purposes of the PEA. One geotechnical hole in the North Zone was also excluded, leaving 68 holes included in the PEA - 47 in the North, and 21 in the South.

The PEA showed 4.6 Blb of copper equivalent (CuEq) in the Indicated category, strictly in the North Zone, with an average grade of 0.37%. In the Inferred category, there is 4.2 Blb of CuEq in the North and South zones combined, with an average grade of 0.34%.

If your high school didn’t offer Mining 101, the Indicated category means there is a moderately high degree of confidence, enough to support mine planning and the evaluation of the economic viability of the resource. Inferred is a lower degree of confidence than Indicated, and means this part of the resource only has limited sampling and information available. In simpler terms, there is not enough information available for the minerals in the Inferred category because the drill holes were likely too far apart to have a high degree of confidence.

This might sound negative, but it isn’t. It means Oroco hasn’t done enough drilling in certain areas to reach the standard of Indicated. As they do more drilling, more areas can be moved from Inferred to Indicated.

The below chart might shed some light on why the minerals in the South Zone are in the Inferred category while much of the North Zone is considered Indicated. There were only 21 holes drilled in the South Zone while the North Zone had 47, many of them close together, allowing for a greater degree of confidence.

VALUATION

Finally, the moment you’ve all been waiting for - what’s it worth? The PEA returned an after-tax NPV8% of US$1.2B and an IRR of 17.3%. Oroco’s 85.5% stake represents about US$1B of that, and similar mines sell for about 50% of the NPV. That means Oroco’s stake could sell for about US$500M (C$675M), and the current market cap is around US$90M (C$120M). Oroco trades for 18% of the potential selling price of its stake in Santo Tomas.

Cantor Fitzgerald covers the company and they use a discounted cash flow model with an 8% discount rate. Their model shows Oroco’s stake in the mining assets are worth about US$706M today, and then they apply a 0.4x discounted NAV multiple to get their price target of US$1.16 per share, or about C$1.60. Oroco trades for about C$0.50 as of this writing.

WHAT’S NEXT FOR SANTO TOMAS

The Phase II drill program planning is underway. This phase will be shorter and less expensive than Phase I, and they’ve raised money recently to partially fund this program.

We are eagerly waiting for more drill program details to be released, but it will aim to fill in some of the gaps in the South Zone to turn waste rock into mineable material, expanding the value of the resource. This will move the project closer to a pre-feasibility study, which is the next big milestone.

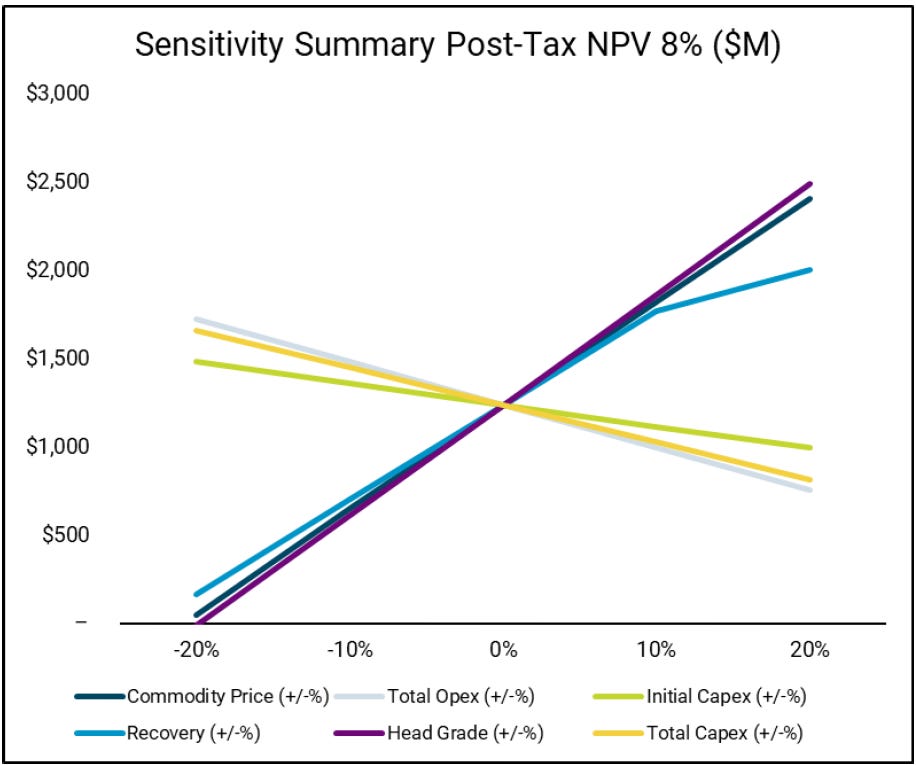

UPSIDE POTENTIAL - SENSITIVITY TO COPPER PRICE

The chart below from Oroco’s PEA shows how sensitive the NPV is to the price of copper and the other commodities at Santo Tomas. Increasing the commodity price input by 10% would increase the post-tax NPV to US$1.8B, a 50% increase. Of course, if commodity prices decline it will negatively impact the NPV to a similar degree.

The impact of this chart likely depends on your view on the future price of copper. I am not a copper expert, but there are people smarter than I am projecting an imminent copper deficit. Copper is a necessary material in the green energy transition, and the supply shortage could come at the same time as EV demand increases the need for copper, driving up the price. This isn’t why I’m invested in Oroco, I believe it is undervalued regardless if copper moves or not, but it helps the upside potential. Below are a couple charts from Goldman Sachs on copper supply.

KEY PERSONNEL

Richard Lock, CEO - Has led the construction and development of several large mining projects around the world. He most recently was senior vice-president of PolyMet Mining Corp. and Project Director for its NorthMet Project in Minnesota. Mr. Lock has held executive and project director roles at notable projects such as Rio Tinto’s Resolution and Keystone copper projects in Arizona and Utah, and Arizona Mining Inc.’s Hermosa project.

Ian Graham, President - Mr. Graham is an accomplished mining professional with over 20 years of experience in the development and exploration of mineral deposits, mostly gained with major mining companies Rio Tinto and Anglo American, including as Chief Geologist with the Project Generation Group at Rio Tinto. Mr. Graham has been involved with evaluation and pre-development work on several projects in Canada and abroad.

Adam Smith, Corporate Finance - Mr. Smith is a co-founder of Altamura Copper Corp. and has been with Oroco since its formation in 2006. He works in business development and corporate finance for Oroco, and his most significant role is working with investment partners to raise money for Oroco to fund the drilling program and operations.

A QUICK RANT

The bottom is in. After the PEA was released, investors heard that more drilling is coming and the company needs to raise money to do so, and they had unrealistic expectations about when Santo Tomas will be sold. They don’t want to hold Oroco throughout 2024 and 2025 because they’re afraid what the market will do in the meantime.

I'm staying invested because I believe Santo Tomas is undervalued relative to Oroco's current share price, and I see a strong potential reward compared to the risks involved. No matter what the economy does, the world still needs more copper, and Santo Tomas is one of the best options for major mining companies to acquire.